Consider a function \(f : \R^n \to \R_+\) that can be written as a sum of a large number

of functions \(f = f_1 + f_2 + \cdots\) from some class. When can this sum be

sparsified in the sense that f can be approximated by a (nonnegative) weighted

combination of a small number of the \(\{f_i\}\)? For many classes of functions, the

answer is that, surprisingly, only about \(O(n)\) summands suffice (up to

logarithmic factors). When this is possible, one can address the algorithmic

questions: How to efficiently construct the sparsifier, and how to use sparse

representations to optimize \(f\) efficiently.

This simple question has a wealth of applications in CS (especially in big

data analysis), as well as in many areas of mathematics (especially in

functional analysis and convex geometry). The course will focus on the

mathematical structures underlying sparsification problems, covering

things like: Leverage scores, Lewis weights, generalized linear regression,

spectral sparsification of graphs, matrix concentration, generic chaining

theory, subspace embeddings and dimension reduction, submodularity, and

low-rank approximation in numerical linear algebra.

Consider the prototypical problem of least-squares linear regression: Suppose we are given input pairs

\((a_1,b_1), (a_2,b_2) \ldots, (a_m,b_m)\) with \(a_1,\ldots,a_m \in \R^n\) and \(b_1,\ldots,b_m \in \R\),

and we want to find \(x \in \R^n\) such that \(\langle a_i,x\rangle \approx b_i\) for all \(i=1,\ldots,m\).

Let \(A\) be the \(m \times n\) matrix whose rows are \(a_1,\ldots,a_m\).

We will assume that the data is noisy and the system is overdetermined (\(m \gg n\)) so that there is no actual solution to \(Ax=b\).

In this case, a natural thing to try is to minimize the least-squares error:

\[\textrm{minimize}\ \left\{ \|Ax-b\|_2^2 : x \in \R^n \right\}.\]

One might now ask the question of whether we really need to work with all \(m\) examples

given that the dimensionality is only \(n \ll m\). Here’s one possible formulation of this problem:

Is there a matrix \(\tilde{A}\) with \(\tilde{m} \approx n\) rows and such that the solution

to any least-squares regression problem with \((\tilde{A},b)\) is close to the solution with \((A,b)\)?

Even more ambitiously, we could ask that every row of \(\tilde{A}\) is a weighted scaling of some row of \(A\).

Thus \(\tilde{A}\) would correspond to the weighted input \(c_{i_1} (a_{i_1}, b_{i_1}), c_{i_2} (a_{i_2}, b_{i_2}), \ldots, c_{i_M} (a_{i_M}, b_{i_M})\),

with \(c_{i_1}, c_{i_2}, \ldots \geq 0\),

and the property we’d like to have is that \(\|A x - b\|_2 \approx \|\tilde{A} x - b\|_2\) for every \(x \in \R^n\).

Sparsification

This is a special case of a general type of sparsification problem: Suppose that $F : \R^n \to \R_+$ is given by

for some nonnegative weights \(c_1,c_2,\ldots,c_m \geq 0\). Say that the representation is \(s\)-sparse if at

most \(s\) of the weights are nonzero. Say that \(\tilde{F}\) is an \(\e\)-approximation to \(F\) if it holds that

\[|F(x)-\tilde{F}(x)| \leq \e F(x),\quad \forall x \in \R^n\,.\]

General linear models

Our least-squares regression problem corresponds to the case where \(f_i(x) = \abs{\langle a_i,x\rangle - b_i}^2\) for \(i=1,\ldots,m\).

$\ell_p$ loss. But one can imagine many other loss functions. If, instead, we took \(f_i(x) = \abs{\langle a_i,x\rangle - b_i}^p\), the corresponding

problem is called $\ell_p$ regression. Jumping ahead:

It is known that for \(p=1\), there are \(s\)-sparse \(\e\)-approximations with \(s \leq O(\frac{n}{\e^2} \log n)\). [Tal90]

For \(1 < p < 2\), there are \(s\)-sparse \(\e\)-approximations with \(s \leq O(\frac{n}{\e^2} \log n (\log \log n)^2)\).

[Tal95]

For \(0 < p < 1\), there are \(s\)-sparse \(\e\)-approximations with \(s \leq O(\frac{n}{\e^2} (\log n)^{3})\).

[SZ01]

For \(p > 2\), it must be that \(s\) grows like \(n^{p/2}\) (and this is tight).

[BLM89]

Moreover, for \(p = 2\), a remarkable fact is that one can do even better: \(s \leq O(n/\e^2)\).

[BSS14]

In general, one can ask the question: Suppose that \(f_i(x) \seteq \varphi(\langle a_i,x\rangle - b_i)\).

For what loss functions \(\varphi : \R \to \R_+\) is such sparsification possible?

Huber and \(\gamma_p\) losses.

An interesting example is the Huber loss where \(\varphi(y) = \min(y^2, |y|)\). (The Huber

loss is more general, but this special case captures its essence.)

The loss function grows quadratically near \(0\), but is much less sensitive to outliers than the \(\ell_2\) loss.

In general, functionals that grow like \(\varphi(y) = \min(y^2, |y|^p)\) for \(0 < p \leq 2\) have been studied,

especially in the context of fast algorithms for solving \(\ell_p\) regression to high accuracy (see, e.g., [BCLL17]).

The best published work achieves \(s \leq O(n^{4-2\sqrt{2}})\) [MMWY21], but we will see, using methods in this course (from

upcoming joint work with Jambulapati, Liu, and Sidford) that \(s \leq O(\frac{n}{\e^2} (\log n)^{O(1)})\) is possible.

What about the function \(\varphi(y) = \min(y^2, 1)\)? This is sometimes called the Tukey loss,

where we know only partial answers to the sparsification question.

ReLUs. For an example of a loss function that doesn’t allow sparsification, consider \(\varphi(y) = \max(0, y - 0.5)\).

The functional \(f_i(x) = \max(0, \langle a_i,x\rangle - 0.5)\) “lights up” only when \(\langle a_i,x\rangle\) is substantial.

But one can easily choose exponentially many unit vectors \(\{a_i\}\) in \(\R^n\) where these functionals have disjoint support,

meaning that there is no way to sparsify down to fewer than a number of terms that’s exponential in the dimension.

If we choose \(f_i(x) = \max(0, |\langle a_i,x\rangle| - 0.5)\), then \(f_1,\ldots,f_m\) are symmetric and convex, so those

two conditions alone are not enough to give strong sparsification.

In general, we don’t yet a complete theory of sparsification even for 1-dimensional functions.

Graph sparsification

Consider an undirected graph \(G=(V,E,w)\) with nonnegative weights \(w : E \to \R_+\) on the edges.

Let us enumerate the edges of \(G\) as \(u_1 v_1, u_2 v_2, \ldots, u_m v_m\), and define

\(f_i(x) = w_{u_i v_i} |x_{u_i} - x_{v_i}|\). Then,

and for \(x \in \{0,1\}^V\), the latter sum is precisely the total weight of the edges

crossing the cut defined by \(x\).

Now the question of whether \(F\) admits an \(s\)-sparse \(\e\)-approximation is precisely the

question of whether the weighted graph \(G\) admits a cut sparsifier in the sense of Benczur and Karger.

If we instead define \(f_i(x) = w_{u_i v_i} |x_{u_i}-x_{v_i}|^2\), then the question becomes one

about spectral graph sparsifiers in the sense of Spielman and Teng.

High-dimensional sparsification

Hypergraph cut sparsifiers. Suppose now that \(H=(V,E,w)\) is a weighted hypergraph in the sense that each hyperedge \(e \in E\)

is a subset of vertices. If we define, for \(e \in E\),

Symmetric submodular functions. More generally, we can ask about the setting where \(f_1,\ldots,f_m : \R^n \to \R_+\) are symmetric submodular functions

and

(More precisely, one should take each \(f_i\) to be the Lovasz extension of a symmetric submodular function with \(f_i(\emptyset) = 0\).)

For \(p=1\), this generalizes the setting of hypergraph cut sparsifiers,

and one can achieve \(s \leq \frac{n}{\e^2} (\log n)^{O(1)}\).

For \(p=2\), the best-known bound is \(s \leq \frac{n^{3/2}}{\e^2} (\log n)^{O(1)}\), and it’s unknown whether one can do better.

General submodular functions. For more general (non-symmetric) submodular functions, there are many classes

of functions that allow varying degrees of sparsification. See, e.g., [KK23].

Unbiased estimators and importance sampling

Unbiased estimators. A general method to construct sparsifiers is by independent random sampling. Suppose we are in the setting \eqref{eq:F} and

let \(\rho = (\rho_1,\ldots,\rho_m)\) be a probability vector, i.e., a nonnegative vector with \(\rho_1 + \cdots + \rho_m = 1\).

Let us sample indices \(i_1,i_2,\ldots,i_M\) i.i.d. from \(\rho\) and define the random sparsifier \(\tilde{F}\) by

and therefore \(\E[\tilde{F}(x)] = F(x)\) as well.

Importance. As we just argued, \(\tilde{F}(x)\) is an unbiased estimator for any \(\rho\), but crucially in order to choose \(M\) small

and still hope that \(\tilde{F}\) will be a good approximation to \(F\), we need to choose \(\rho\) carefully.

A simple example comes from the \(\ell_2\) regression problem. Let us assume that \(b=0\) and consider \(a_1,\ldots,a_m \in \R^n\) such that \(a_1\) is linearly

independent from \(a_2,\ldots,a_m\). Then \(f_1(x) = |\langle a_1,x\rangle|^2\) must appear in a sparse approximation to \(F\) to handle the input \(x = a_1\).

Therefore we will need to sample at least \(O(1/\rho_1)\) terms before we expect to have \(f_1\) appear.

If we are looking to have \(M \leq n (\log n)^{O(1)}\), it’s clear that choosing \(\rho\) to be uniform, for instance, will be drastically insufficient.

Concentration. In general, once we choose \(\rho\), we are left with the non-trivial problem of getting \(F(x) \approx \tilde{F}(x)\)

for every \(x \in \R^n\). This can be a daunting task that is often framed as bounding an expected maximum:

\(\ell_2\) regression and statistical leverage scores

Considering \(F(x) = f_1(x) + \cdots + f_m(x)\), one way to choose an importance for each \(f_i\) is to obtain

a uniform bound on each term. In other words, we consider the quantity

\[\alpha_i \seteq \max_{0 \neq x \in \R^n} \frac{f_i(x)}{F(x)}\,.\]

If we assume that \(F\) and \(f_i\) scale homogeneously (e.g., in the case of \(\ell_2\) regression, \(F(\lambda x) = |\lambda|^2 F(x)\) and

similarly for each \(f_i\)), then we can write this as

for \(a_1,\ldots,a_m \in \R^n\), and we define \(A\) as the matrix with \(a_1,\ldots,a_m\) as rows.

We’ll derive our importance scores in a few different ways. Each of these perspectives will be useful

for moving later to more general settings.

Uniform control.

Consideration of \eqref{eq:uniform-con} in this setting is easy:

therefore our corresponding sample probabilities would be \(\rho_i \seteq \sigma_i(A)/\mathrm{rank}(A)\).

We will assume in the rest of this lecture that \(\mathrm{rank}(A) = n\), but this is only for convenience.

Symmetry considerations.

We have already seen that if \(a_1\) is linearly independent

from the rest of the vectors, then we should sample it with a pretty large probability (considering the case where \(a_1,\ldots,a_n\)

forms an orthonormal basis, “large” will have to mean probability \(\approx 1/n\)).

Another indication comes from how \(F\) scales: If we replace \(a_1\) by two copies of \(a_1/\sqrt{2}\), then the function \(F\) doesn’t change.

This suggests that \(\rho_i\) should scale proportional to \(\|a_i\|_2^2\).

But notice also that \(F\) is a sum of squares; as there are no cancellations, it is natural to consider

the matrix \(a_1 a_1^{\top} + \cdots + a_m a_m^{\top} = A^{\top} A\). Let’s suppose, for simplicity, that

the vectors form a decomposition of the identity:

Then we have \(\|a_1\|_2^2 + \cdots + \|a_m\|_2^2 = \tr\left(a_1 a_1^{\top} + \cdots + a_m a_m^{\top}\right) = \tr(I) = n\), so symmetry suggests

we take \(\rho_i \seteq \|a_i\|_2^2/n\).

For the general case, let us assume that \(A\) has full rank, i.e., \(\mathrm{rank}(A) = n\).

We can left-multiply the vectors by \((A^{\top} A)^{-1/2}\) to achieve \eqref{eq:isotropic}, again suggesting the

probabilities \(\rho_i = \sigma_i(A)/n\).

We can think about leverage scores in a couple of other ways.

Expected contribution to \(F(x)\).

One way to judge the importance of \(a_i\) is to switch from a “worst case” perspective (approximating \(F(x)\) for every \(x\))

to an ``average case’’ one: Suppose that \(\mathbf{X}\) is a random vector in \(\R^n\) and define

What distribution should we use? In the case that \eqref{eq:isotropic} holds, it makes sense for \(\mathbf{X}\) to be rotationally

invariant, and indeed any such choice works. Using the Gaussian measure on $\R^n$, this would give

and it is straightforward to check that \(\rho_i \propto \|a_i\|_2^2\). And if we apply the

transformation \((A^{\top} A)^{-1/2}\) to a general set of vectors to achieve \eqref{eq:isotropic}, then the corresponding

form is

and again one has \(\rho_i \propto \|(A^{\top}A)^{-1/2} a_i\|_2^2\).

Singular value decomposition.

Suppose we write \(A = U \Sigma V^{\top}\). Recall that we consider \(n \leq m\), thus \(\Sigma = \begin{bmatrix} D \\ \hline 0\end{bmatrix}\),

where \(D\) is an \(n \times n\) diagonal matrix containing the singular values \(\sigma_1,\ldots,\sigma_n\).

Note that \(U\) is an \(m \times m\) matrix, but \(\Sigma\) makes all but the first \(n\) columns of \(U\) meaningless (indeed,

one can obtain an SVD from any completion of the first \(n\) columns of \(U\) to an orthonormal basis).

If we consider the “compact SVD” \(A = \hat{U} \Sigma V^{\top}\) where we cut the last \(m-n\) columns off of \(U\), then \(\sigma_i(A) = \|\hat{u}_i\|_2^2\),

where \(\hat{u}_1,\ldots,\hat{u}_m\) are the rows of \(\hat{U}\).

Concentration

Once we’ve chosen our sampling probabilities \(\rho_i = \sigma_i(A)/n\), we can independently sample \(M\) terms

from the distribution, and we are left to analyze the random sum

We have already argued that \(\E[\tilde{A}] = A\), so the real question is about concentration, which we will begin to cover

in the next lecture.

There are actually two ways to approach this question. One is to think about proving concentration of the sum along every direction \(x \in \R^n\)

simultaneously. This leads naturally to entropy bounds, covering numbers, and the generic chaining theory.

The second approach is to think about \(\tilde{A}\) as a random operator and try to prove concentration of sums of independent random matrices.

The former will be far more general, while the latter appears substantially more powerful in certain special cases.

Recall that we have a function \(F : \R^n \to \R\)

written as \(F(x) = f_1(x) + \cdots + f_m(x)\) and we want to sparisfy it by

sampling the terms in proportion to a probability vector \(\rho \in \R_+^m\) (the “importance scores”).

One way to analyze this is to first make sure all the probabilities are uniformly small, say \(\rho_1,\ldots,\rho_m \leq 2/m\).

Since we are trying to sparsify down to a number of terms that is independent of \(m\), we can always achieve

this by simply splitting a term

Then one can sparsify in phases by deleting every term independently with probability \(1/2\). This experiment can be modeled

with \(\{0,1\}\) random variables in the natural way:

where \(\e_1,\ldots\e_m\) are i.i.d. uniform random $\pm 1$ variables, and \(\Omega \subseteq \R^n\) is our domain of interest.

It turns out that it is possible to do something similar and reduce the analysis of one-shot sampling

to the analysis of randomly signed sums of the functions. This makes for both a simpler algorithm,

and a more robust method of analysis that will be very useful later.

Symmetrization, take II

Let’s consider a more general situation. Consider a family of independent random functions \(\mathbf{g}_1,\ldots,\mathbf{g}_M : \R^n \to \R\)

that are sampled from some distribution. (Recall that we are thinking about each one as being chosen from a finite family of functions and, in our case,

it even holds that they are i.i.d.).

Define \(\mathbf{G}(x) \seteq \mathbf{g}_1(x) + \cdots + \mathbf{g}_m(x)\) and \(F(x) \seteq \E[\mathbf{G}(x)]\).

We are interested in the quantity

where \(\delta < 1\). Then we have \(\mathcal{S} \lesssim \delta\).

Proof: Note that if \(\tilde{\mathbf{g}}_1, \ldots, \tilde{\mathbf{g}}_M\) is an independent family of functions from the same distribution, then

clearly \(F(x) = \E\left[\tilde{\mathbf{g}}_1(x) + \cdots + \tilde{\mathbf{g}}_M(x)\right]\) as well, so we can write

and note that since \(\mathbf{g}_i(x) - \tilde{\mathbf{g}}_i(x)\) and \(\tilde{\mathbf{g}}_i(x)-\mathbf{g}_i(x)\) have the same distribution, we can write this as

Given the above discussion and recalling the definition in \eqref{eq:Esup}, if \eqref{eq:rad} holds for every choice of \(g_1,\ldots,g_M\), this yields the bound

where the last inequality uses concavity of the square root to move the expectation inside.

For \(\delta < 1\), this tells us that \(\mathcal{S} \leq O(\delta)\).

This completes the symmetrization argument, allowing us to focus on proving bounds like \eqref{eq:rad}.

The advantage here lies in the the fact that \(\left \{ \e_1 g_1(x) + \e_2 g_2(x) + \cdots + \e_M g_M(x) : x \in \R^n \right\}\)

is an example of a subgaussian process, and bounding the expected maximum of a subgaussian process has a long and rich history,

along with a correspondingly powerful framework.

The (mild) disadvantage is that we require the inequality \eqref{eq:rad} to hold for every choice of functions \(g_1,\ldots,g_M\)

in the support of our distribution.

(Note: The confusing terminology “process” is a historical artifact. Originally,

one was indeed interested in \(\e_1 g_1(x)\), \(\e_1 g_1(x) + \e_2 g_2(x)\), etc. as a sequence “evolving in time.”

If one switches from discrete to continuous time, e.g., a process like Brownian motion, then control of the

expected maximum is closely related to almost sure continuity of the sample paths.)

Subgaussian processes

Consider a collection of random variables \(\{ X_t : t \in T \}\) where the index set \(T\) is

equipped with a distance \(d\).

The family is called subgaussian (with respect to \(d\)) if there

if there is a constant \(c > 0\) such that

Gaussian processes. The canonical example occurs when \(\{X_t : t \in T\}\) is a jointly Gaussian family of random variables,

in which case \eqref{eq:subgaussian} holds with \(c=1/2\) and \(d(s,t) = (\E |X_s-X_t|^2)^{1/2}\).

Note that if the index set \(T\) is finite, then such a family can always be realized in the following way:

Let \(g_1,g_2,\ldots,g_m\) be i.i.d. \(N(0,1)\) random variables and define

\(X_t = t_1 g_1 + t_2 g_2 + \cdots + t_m g_m\) for \(t \in T \subseteq \R^n\).

Bernoulli processes. Suppose that \(\e_1,\ldots,\e_m\) are i.i.d uniform \(\pm 1\) random variables and for \(t \in T\), we define

\(X_t \seteq \e_1 t_1 + \e_2 t_2 + \cdots + \e_m t_m\). Then the \(\{ X_t : t \in \R^n \}\) is a family

of subgaussian random variables with the same parameters: \(c=1/2\) and \(d(s,t) = (\E |X_s-X_t|^2)^{1/2}\).

Many proofs are known. Even proofs of significant generalizations can be made quite short. See, e.g., the proof of Theorem 1.3 here.

The quantity we care about after our symmetrization argument is

and as we have just seen this is the expected maximum of a centered subgaussian process. (Centered means that \(\E X_t = 0\) for every \(t \in T\).)

There is a rich history and theory for

bounding such expected maxima, with M. Talagrand as the primary architect (see his comprehensive book on the topic).

Suppose now that \(\{ X_t : t \in T \}\) is subgaussian with respect to the distance \(d\).

Our goal is to get some control on \(\E \max_{t \in T} X_t\), and one of the central tenants

of the theory is that we can do this using just the geometry of the distance \(d\).

Let’s suppose that \(d\) is symmetric \(d(s,t)=d(t,s)\) for all \(s,t \in T\), and that it

satisfies the triangle inequality:

Define the quantity \(e_h(T,d)\) as the smallest radius \(r\) such that \((T,d)\) can be

covered by at most \(2^{2^h}\) balls of radius \(r\), where a ball in \((T,d)\) is given by

\[B(t, r) \seteq \{ s \in Y : d(s,t) \leq r \}\,.\]

It follows by a greedy construction

that there exists a “net” \(N_h \subseteq T\) such that \(|N_h| \leq 2^{2^h}\) and

every point of \(T\) is within distance at most \(e_h(T,d)\) of a point in \(N_h\).

It is useful to think of \(N_h\) as the “best” uniform approximation of \((T,d)\) when

one is only allowed to use \(2^{2^h}\) points.

Let’s fix any such sets \(\{N_h : h=0,1,2,\ldots\}\).

Let \(\pi_h : T \to N_h\) be a map that satisfies

\[\begin{equation}\label{eq:pih}

d(t, \pi_h(t)) \leq e_h(T,d)\,\qquad \forall t \in T\,.

\end{equation}\]

For instance, a natural choice is for \(\pi_h(t)\) to map \(t\) to the closest point of \(N_h\),

but we will only need \eqref{eq:pih}.

If we think about \(U_h\) as containing “edges” that gets stretched to random lengths,

then this event entails no edge of \(U_h\) being stretched too much.

Since every pair in \(U_h\) is within distance \(2 e_h(T,d)\), a union bound combined with \eqref{eq:subgaussian} gives

where we have used the obvious bound \(\abs{U_h} \leq \abs{N_h} \abs{N_{h+1}}\) and the fact that \(\abs{N_h} \abs{N_{h+1}} \leq 2^{2^h} 2^{2^{h+1}}\).

A natural choice is now \(\lambda \seteq 4 \frac{\alpha}{c} 2^{h/2}\) for some number \(\alpha > 0\) we will choose later.

If we define \(\mathcal{E}_h \seteq \mathcal{E}_h((\alpha/c) 2^{(h+2)/2})\), then the preceding bound gives us

Note that the leading constant is not so important, we just wanted a clean form for the lower bound. The

real point here is that \(\lambda\) is scaling like \(2^{h/2}\), and the probability of \(\mathcal{E}_h\)

not occurring can be summed over all \(h \geq 0\), since it’s doubly geometric.

If we now simply take a union bound over \(h=0,1,2,\ldots,\), we get

We’ve gone through all this effort because it turns out that if \(\mathcal{E}_h\) holds for every \(h \geq 0\), it gives

us a bound on \(\E \max_{t \in T} (X_t - X_{t_0})\), where \(\{t_0\} = N_0\) (note that \(N_0\) could be any fixed point of \(T\)).

The argument goes via chaining. Consider first the infinite telescoping sum

If we think of this as a chain, then every link in the chain is going to lie in some set \(U_h\), and thus having

control on the stretch of all the “edges” we considered previously will give us control on every term in this chain.

You can assume the sum is finite if you like, because

which goes nicely with our goal of bounding \eqref{eq:delta-bound} via \eqref{eq:dudley}.

Bounding the entropy numbers.

For a metric space \((T,d)\), define \(\mathcal{N}(T,d,\e)\) as the minimal number of \(\e\)-balls

in \((T,d)\) needed to cover \(T\).

It will help to check one’s understanding of the definitions to verify that if

where \(B_2^n\) is the unit ball in the Euclidean norm.

Sparsifiers for \(\ell_2\) regression.

Let us first use the Covering Lemma to finish our first construction of sparsifiers for \(\ell_2\) regression.

Recall that we choose \(\rho_{i} \seteq \|(A^{\top} A)^{-1/2} a_i\|_2^2/n\), where \(A\) is the matrix

with rows \(a_1,\ldots,a_m\) and, in this case, \(F(x) = \|Ax\|_2^2\).

Using the linear transformation \(x \mapsto (A^{\top} A)^{-1/2} x\), we can write

where \(U\) is the matrix with rows \(u_j \seteq \frac{(A^{\top} A)^{-1/2} a_{\nu_j}}{\sqrt{M \rho_{\nu_j}}}\).

Note that, by our choice of \(\rho_1,\ldots,\rho_M\), we have

where the last inequality holds for the unit ball of any norm on \(\R^n\) (and, indeed, \(d_{\nu,\infty}\)

is a distance induced by a norm on \(\R^n\)), as you show in Homework #1.

Putting everything together. Now \eqref{eq:ent1} and \eqref{eq:ent2} in conjunction give

Therefore by setting \(M \seteq C \frac{n}{\e^2} (\log n)^2 \log(n/\e)\) for an appropriate constant \(C > 1\),

\eqref{eq:Fapprox} gives us our desired \(\e\)-approximation.

The covering lemma

Before proving the lemma, it helps to consider the more basic problem of covering the Euclidean

ball \(B_2^n\) by translates of \(\e B_{\infty}^n\), i.e., by translates of small cubes.

Suppose \(\|x\|_2^2 = x_1^2 + x_2^2 + \cdots + x_n^2 = 1\). Since we only care about approximation

up to \(\e\) in the \(\ell_{\infty}\) distance, we could discretize this vector to lie in, say,

\(\e \mathbb{Z}^n \cap B_2^n\).

The most basic kind of vector we need to cover is of the form

\((0, \pm \e, 0, 0, \pm \e, 0, \pm \e, 0, \ldots, 0)\). Because \(\|x\|_2^2 = 1\), there

are only \(n^{O(1/\e^2)}\) choices for such a vector.

But we also need to handle vectors of the form \((0, \pm 2\e, 0, 0, \pm \e, 0, \pm 2\e, 0, \ldots, 0)\), and so on.

It is not hard to convince one’s self that there are asymptotically fewer vectors of this form.

Ineed, if some entry is \(2\e\) then there are \(n\) choices for where it goes, but there are \(n(n-1)/2\) choics

for where two copies of \(\e\) go. Thus the total number of centers one needs is only \(n^{O(1/\e^2)}\).

Now suppose we wanted to cover \(B_2^n\) instead with cubes of different side lengths, or with parallelpipeds

(where the sides are no longer perpendicular), etc. There is a beautiful approach that gives surprisingly good

bounds for cover \(B_2^n\) by translations of an arbitrary symmetric convex body.

(I have heard it credited to Talagrand, or to Pajor and Talagrand.)

The dual-Sudakov approach.

We will prove the following substantial strengthening of this bound.

Suppose that \(d(x,y) = \|x-y\|\) is a distance induced by some norm $\norm{\cdot}$ on \(\R^n\).

Then for every \(\e > 0\),

The last bound is a basic exercise with the gaussian tail, taking a union bound over the \(M\)

gaussian variables \(\{ \langle u_j,\mathbf{g} \rangle : j \in [M] \}\).

Shift Lemma: Suppose that \(\gamma_n\) is the standard gaussian measure on \(\R^n\)

and \(W \subseteq \R^n\) is any symmetric set (\(W = -W\)) and \(z \in \R^n\). Then,

Let \(B \seteq \{ x \in \R^n : \|x\| \leq 1 \}\) denote the unit ball in our given norm.

By scaling, we can assume that \(\e = 2\).

If we cannot cover \(B_2^n\) by \(N\) translates of \(2 B\), then there must exist

\(x_1,\ldots,x_N \in B_2^n\)

such that \(x_1 + B, \ldots, x_N + B\) are all pairwise disjoint.

Let \(\lambda > 0\) be a parameter we will choose momentarily, and note that

\(\lambda (x_1+B),\ldots, \lambda(x_N+B)\) are pairwise disjoint as well, therefore

\[\begin{align*}

1 \geq \gamma_n\left(\bigcup_{i \leq N} \lambda (x_i+B)\right) &= \sum_{i \leq N} \gamma_n\left(\lambda (x_i+B)\right) \\

&\geq \gamma_n(\lambda B) \sum_{i \leq N} e^{-\lambda^2 \|x_i\|_2^2/2} \\

&\geq \gamma_n(\lambda B) N e^{-\lambda^2/2}\,,

\end{align*}\]

where the first inequality uses the Shift Lemma and the second inequality uses \(x_1,\ldots,x_N \in B_2^n\).

Now note that, by Markov’s inequality, \(\E \|\mathbf{g}\| \geq \lambda \gamma_n(\R^n \setminus (\lambda B))\),

thus taking \(\lambda \seteq 2 \E \|\mathbf{g}\|\) gives \(\gamma_n(\lambda B) \geq 1/2\), and we conclude that

Fix \(1 \leq p \leq 2\).

We will now prove that if \(a_1,\ldots,a_m \in \R^n\)

and \(f_i(x) = |\langle a_i,x\rangle|^p\), then the sum

\(F(x) = f_1(x) + \cdots + f_m(x)\) admits \(s\)-sparse \(\e\)-approximations for

$$

s \lesssim \frac{n}{\e^2} \left(\log \frac{n}{\e}\right)^{O(1)},

$$

generalizing what we saw last lecture for \(p=2\).

As we have already seen, this will follow from an estimate of the form

Let \(B_N\) denote the unit ball of \(N\).

Define \(V(r) \seteq \mathrm{vol}_n(r B_N) = r^n \mathrm{vol}_n(B_N)\) so that \(\frac{d}{dr} V(r) = n r^{n-1} \mathrm{vol}_n(B_N)\).

Therefore,

where the latter equality follows from integration by parts.

Let \(\mathbf{Z}\) be a random variable with law \(\mu\), where \(\mu\) has density proportional to \(e^{-\norm{Ax}_p^p}\).

Then the lemma tells us that

Check that in the case \(p=2\), it holds that \(\rho_i = \norm{(A^{\top} A)^{-1/2} a_i}_2^2/n\), i.e.,

the corresponding weights are precisely the statistical leverage scores.

The shift lemma and uniform smoothness

In light of our choice of important scores in \eqref{eq:lp_scores}, we can think of the following setting.

Let \(U\) be a matrix with rows \(u_1,\ldots,u_M \in \R^n\).

Let \(\mathbf{Z}\) be a random variable whose distribution has density proportional to \(e^{-\|A x\|_p^p}\),

and assume that

Note that if \(u_j = a_{\nu_j}/(M \rho_{\nu_j})^{1/p}\), then \(K \leq (\frac{n}{p M})^{1/p}\) using \eqref{eq:rho-alt}.

Our goal now is to bound the covering numbers of the set \(B_A \seteq \{x \in \R^n : \|A x\|_p \leq 1 \}\)

in the metric \(d_{U}(x,y) \seteq \|U(x-y)\|_{\infty}\).

Recall that we did this in the last lecture in the case \(p=2\) using the Shift Lemma for the gaussian measure.

There we used the inequality

For \(1 \leq p \leq 2\), the \(\ell_p\) norm is \(p\)-uniformly smooth with constant \(1\). This reduces to the \(1\)-dimensional inequality (due to Clarkson):

where the first inequality is concavity of \(y \mapsto y^{q}\) for \(0 \leq q \leq 1\), and the second

inequalitiy uses $(u+v)^q \leq u^q + v^q$ for \(0 \leq q \leq 1\) and \(u,v \geq 0\).

Uniform smoothness is a quantative measure of how much the unit ball of a norm lacks “corners.”

Consider the modulus of smoothness

Then \(N\) is \(p\)-uniformly smooth if \(\rho_N(t) \leq O(t^p)\) for all \(t > 0\).

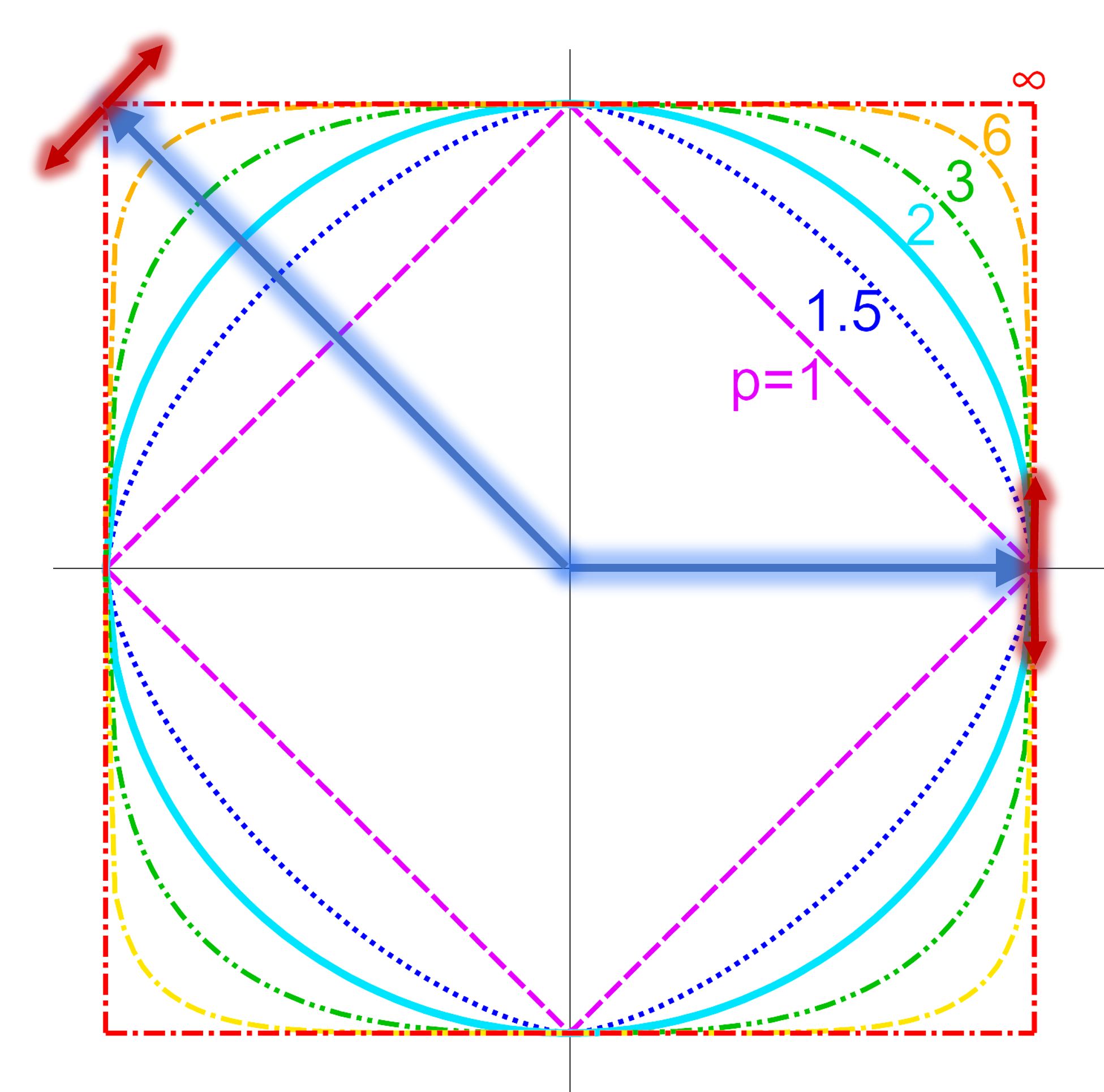

To get some intuition for this notion, see the figure to the right. The blue arrow

corresponds to \(x\) and the red arrows correspond to \(\pm y\). One of the directions

is bad for the \(\ell_1\) ball, and the other for the \(\ell_{\infty}\) ball.

Note how following the red arrows takes one far outside the \(\ell_1\) (and \(\ell_{\infty}\)) ball,

but almost stays inside the \(\ell_2\) ball.

It turns out that \(\ell_p\) is \(p\)-uniformly smooth with constant \(1\) for \(1 \leq p \leq 2\),

and \(2\)-uniformly smooth with constant \(O(\sqrt{p})\) for \(p > 2\).

Shift Lemma for \(p\)-uniformly smooth norms:

Suppose $N$ is a norm on $\R^n$ that is $p$-uniformly smooth with constant $S$. Let \(\mu\)

be the probability measure on \(\R^n\) with density proportional to \(e^{-N(x)^p}\).

Then for any symmetric convex body \(W \subseteq \R^n\) and \(z\in \R^n\),

\[\begin{equation}\label{eq:shift-measure}

\mu(W+z) \geq e^{- S^p N (z)^p}\mu(W)\,.

\end{equation}\]

where the equality uses symmetry of ${W}$, the first inequality uses convexity of $e^y$, and the second inequality

uses $p$-uniform smoothness of $N$ (recall \eqref{eq:p-smooth}).

Dual-Sudakov Lemma for \(p\)-smooth norms.

Let \(N\) and \(\hat{N}\) be norms on \(\R^n\).

Suppose that $N$ is $p$-uniformly smooth with constant $S$,

and let \(\mu\) be the probability measure on $\R^n$ with density

propertional to \(e^{-N(x)^p}\).

Then for any $\e > 0$,

Proof:

By scaling $\hat{N}$, we may assume that $\e = 1$.

Suppose now that $x_1,\ldots,x_M \in B_{N}$ and $x_1+B_{\hat{N}},\ldots,x_M+B_{\hat{N}}$ are pairwise disjoint.

To establish an upper bound on $M$, let $\lambda > 0$ be a number

we will choose later and write

Since it holds that \(\E[\abs{\langle u_j,\mathbf{Z}\rangle}] \leq \left(\E \abs{\langle u_j,\mathbf{Z}\rangle}^p\right)^{1/p} \leq L^{1/p}\) by \eqref{eq:pth-moments},

we are left with the final piece, a concentration estimate for the random variables \(\{ \langle u_j, \mathbf{Z} \rangle \}\).

\(\psi_1\) concentration for one-dimensional marginals of log-concave measures

Exponential concentration. Let’s first summarize the final piece: The function \(e^{-\|Ax\|_p^p}\) is log-concave, meaning

that the random variable \(\mathbf{Z}\) is log-concave. You will prove in HW#2 that the \(1\)-dimensional marginals of such a random variable always satisfy an exponential concentration inequality: For some constant \(c > 0\),

\[\P\left[\abs{\langle u_j, \mathbf{Z}\rangle} \geq t \E[\abs{\langle u_j, \mathbf{Z}\rangle} \right] \leq e^{-c t}\,,\quad t \geq 1\,.\]

Finishing the argument. In particular, this implies that

And using our symmetrization reduction, we should take \(M \asymp \frac{n}{\e^2} (\log (n/\e))^p (\log n)^2\) to obtain an \(\e\)-approximation

with precisely \(M\) terms.

Claim: Suppose that $U_0$ is a maximizer of \eqref{eq:lewis-opt}. Then,

\((U_0^{\top} U_0)^{-1} = A^{\top} W A\,,\) where $W$ is a nonnegative

diagonal matrix with $W_{ii} = \norm{U_0 a_i}_2^{p-2}$ for $i=1,\ldots,m$.

Proof: The method of Langrange multipliers tells us that there is a nonnegative

$\lambda > 0$ such that the maximum is given by a critical point of the

functional

Assuming that $\mathrm{span}(a_1,\ldots,a_m) = \R^n$, it is

straightforward to check that the optimization has a finite, non-zero

maximum, and therefore any maximizer $U_0$ is invertible.

Let us compute the gradient of $G(U)$ with respect to the matrix entries

${ U_{ij} : 1 \leqslant i,j \leqslant n }$. The rank-one update rule

for the determinant says that for invertible $U$,

\[\det(U + u v^{\top}) = \det(U) (1+\langle v, U^{-1} u\rangle)\,,\]

This follows from $U + uv^{\top} = U (I + U^{-1} uv^{\top})$,

$\det(AB)=\det(A)\det(B)$, and

$\det(I + uv^{\top}) = 1 + \langle u,v\rangle$.

As before, the analysis of concentration for importance sampling comes

down to analyzing covering numbers of the set

\(B_{A,p} \seteq \{ x \in \R^n : \|Ax\|_p \leqslant 1 \}\)

in the metric

From \eqref{eq:l2-lp}, we see that the Euclidean ball

\(B_{\rho,2} \seteq \{ x \in \R^n : \norm{U^{-1} x}_2 \leq 1 \}\)

satisfies $B_{A,p} \subseteq B_{\rho,2}$.

Denote the unit ball

\(B_{\rho,\infty} \seteq \{ x \in \R^n : \norm{x}_{\rho,\infty} \leqslant 1 \}\).

Then we can bound

\[\mathcal{N}(B_{A,p}, r B_{\rho,\infty}) \leqslant\mathcal{N}(B_{\rho,2}, r B_{\rho,\infty})\,.\]

If we apply the linear transformation $U^{-1}$ that takes $B_{\rho,2}$

to the standard Euclidean ball $B_2$, then the dual-Sudakov inequality

tells us how to bound the latter quantity:

\[\begin{equation}\label{eq:lewis-ds}

(\log \mathcal{N}(B_{\rho,2}, r B_{\rho,\infty}))^{1/2} \lesssim \frac{n^{1/p}}{r} \max_{i=1,\ldots,m} \frac{|\langle U a_i, \mathbf{g}\rangle|}{\|U a_i\|_2}

\lesssim \frac{n^{1/p}}{r} \sqrt{\log m}\,.\end{equation}\]

Problematically, this bound is too weak to recover \eqref{eq:ldb}. Taking both sides to the $p/2$ power gives

\[\begin{equation}\label{eq:badcover}

(\log \mathcal{N}(n^{1/p} B_{\rho,2}, r B_{\rho,\infty}))^{1/p} \lesssim \frac{n^{1/2}}{r^{2/p}} (\log m)^{p/4}\,.\end{equation}\]

The issue is that the scaling in $r$ is bad unless $p=2$ (compare \eqref{eq:ldb}).

The problem is our use of the worst-case bound

$B_{A,p} \subseteq n^{1/p} B_{\rho,2}$. There is a more sophisticated

way to bound covering numbers in this setting using norm interpolation

and duality of covering numbers (see Ledoux-Talagrand, Prop 15.19).

But the sort of improvement one needs can be summarized as follows: \eqref{eq:badcover}

is bad for $r \to 0$, but it gives a good bound

for $r$ small, but constant. Having covered $B_{\rho,2}$ by translates

of $B_{\rho,\infty}$, we get an improved bound on the inner products

$|\langle a_i,x\rangle|^{2-p}$ in \eqref{eq:lewis-exp}

This, in turn, gives us a better bound on

$\norm{U^{-1} x}_2$, which means that when we want to reduce the radius

from $r$ to $r/2$ (say), we get an improved estimate for the Euclidean

diameter, making the application of \eqref{eq:lewis-ds} stronger.

Computation of the Lewis weights for $p < 4$: A contraction argument

For $p < 4$, it is possible to compute the Lewis weights using a simple

iterative scheme, assuming that one can compute leverage scores. For a

matrix $A$, define the $i$th leverage score by

$\sigma_i(A) \mathrel{\mathop:}=\langle a_i, (A^{\top} A)^{-1} a_i\rangle$.

In this section, if $W$ is a nonnegative $m \times m$ diagonal matrix,

we will use $w \in \R_+^m$ for the vector with $w_i = W_{ii}$

for $i=1,\ldots,m$.

Define

$\tau_i(w) \mathrel{\mathop:}=\langle a_i, (A^{\top} W A)^{-1} a_i\rangle$.

The idea is to recall that for the Lewis weights, we have

$w_i = \norm{U a_i}_2^{p-2}$, hence

Finally, define the vector $\tau(w) \in \R_+^m$ by

$\tau(w) \mathrel{\mathop:}=(\tau_1(w),\ldots,\tau_m(w))$.

Claim: For any $w,w’ \in \R_+^m$, it holds that \(d(\tau(w),\tau(w')) \leqslant d(w,w')\,.\)

Proof: If $w_i \leqslant\alpha w’_i$ for every $i=1,\ldots,m$, then

$W \preceq \alpha W’$ in the PSD (Loewner) ordering. Therefore

$A^{\top} W A \preceq \alpha A^{\top} W’ A$, and finally

$(A^{\top} W’ A)^{-1} \preceq \alpha (A^{\top} W A)^{-1}$, since matrix

inversion inverts the PSD order.

Finally, by definition this yields

$\langle u, (A^{\top} W’ A)^{-1} u\rangle \leqslant\langle u, (A^{\top} W A)^{-1} u \rangle$

for every $u \in \R^m$. In particular,

$\tau_i(w’) \leqslant\alpha \tau_i(w)$ for each $i=1,\ldots,m$.

Note that if $1 \leqslant p < 4$, then $|(p-2)/p| < 1$, and therefore

$\varphi$ is a strict contraction on the space of weights. In

particular, it holds that for $\delta > 0$ such that

$1-\delta = |(p-2)/p|$, and any $w_0 \in \R_+^m$,

Our goal will be to sparification where the terms are

$f_i(x) \mathrel{\mathop:}=N_i(x)^p$ in our usual notation, and

$F(x) = N(x)^p$.

A semi-norm $N$ is nonnegative and satisfies

$N(\lambda x) = |\lambda| N(x)$ and $N(x+y) \leqslant N(x)+N(y)$ for all

$\lambda\in \R$, $x,y \in \R^n$, though possibly

$N(x)=0$ for $x \neq 0$.

Note that, equivalently, a semi-norm is a homogeneous function:

$N(\lambda x) = |\lambda| N(x)$ such that $N$ is also convex.

Examples

Spectral hypergraph sparsifiers. Consider subsets

$S_1,\ldots,S_m \subseteq {1,\ldots,n}$ and

Then sparsifying $F(x) = f_1(x) + \cdots + f_m(x)$ is called

spectral hypergraph sparsification.

More generally, we can consider linear operators

${ A_i \in \R^{d_i \times n} }$ and the terms

$f_i(x) \mathrel{\mathop:}=\norm{A_i x}_{\infty}^2$.

Symmetric submodular functions. A function

$f : 2^V \to \R_+$ is submodular if

\[f(S \cup \{v\}) - f(S) \geqslant f(T \cup \{v\}) - f(T)\,,\quad \forall S \subseteq T \subseteq V, v \in V\,.\]

If one imagines $S \subseteq V$ to be a set of items and $f(S)$ to

be the total utility, then this says that the marginal utility of an

additional item $v \in V$ is non-increasing as the basket of items

increases. As a simple example, consider

$w_1,\ldots,w_n \geqslant 0$ and

$f(S) \mathrel{\mathop:}=\min\left(B, \sum_{i \in S} w_i\right)$.

Here, the additional utility of an item drops to $0$ as one

approaches the “budget” $B$.

A submodular function $f : 2^V \to \R_+$ is symmetric if

$f(\emptyset)=0$ and $f(S) = f(V \setminus S)$ for all

$S \subseteq V$. A canonical example is where $f(S)$ denote the set

of edges leaving a cut $(S, V \setminus S)$ in an undirected graph.

The Lovász extension of a submodular function is the function

$\tilde{f} : [0,1]^V \to \R_+$ defined by

where $\mathbf{S}_x$ is a random set such that $i \in \mathbf{S}_x$

with probability $x_i$, independently for every $i \in V$.

Fact: A function $f : 2^V \to \R_+$ is submodular if and only if

$\tilde{f} : [0,1]^V \to \R_+$ is convex.

Because of this fact, it turns out that a function $f$ is symmetric

and submodular if and only if $\tilde{f}$ is a semi-norm, where we

extend $\tilde{f} : \R^V \to \R_+$ to all of

$\R^V$ via the definition

\[\begin{equation}\label{eq:lov-ext}

\tilde{f}(x) \mathrel{\mathop:}=\int_{-\infty}^{\infty} f(\{ i : x_i \leqslant t \})\,dt\,.\end{equation}\]

Note that if \(x \in \{0,1\}^V\) is such that

$x_i = \mathbf{1}_S(i)$, then we have

\[\tilde{f}(x) = \int_{0}^1 f(\{ i : x_i \leqslant t \}\,dt\,,\]

since $f(\emptyset)=f(V)=0$. Moreover,

\(\{ i : x_i \leqslant t \} = S\) for $0 < t < 1$, hence

$\tilde{f}(x)=f(S)$. So $\tilde{f}$ is indeed an extension of $f$. A

similar argument shows that for $x$ defined this way,

$\tilde{f}(-x)=f(V \setminus S)$.

Lemma: A function $f : 2^V \to \R_+$ is symmetric and submodular

if and only if $\tilde{f}$ is a semi-norm.

Proof:

A semi-norm $\tilde{f}$ is convex, and therefore by the fact above,

$f$ is submodular. Moreover $\tilde{f}(0)=0$ and

$\tilde{f}(x)=\tilde{f}(-x)$ for a semi-norm, so if

$x \in {0,1}^V$ is given by $x_i = \mathbf{1}_S(i)$, then

$f(S)=\tilde{f}(x)=\tilde{f}(-x)=f(V\setminus S)$ and thus $f$ is

symmetric.

Conversely, if $f$ is symmetric and submodular, then

$\tilde{f}(x)=\tilde{f}(-x)$ and $\tilde{f}$ is convex. Moreover,

the defintion \eqref{eq:lov-ext}

shows that $\tilde{f}(cx)=c \tilde{f}(x)$

for $c > 0$, hence $\tilde{f}$ is also homogeneous, implying that

it’s a semi-norm.

Thus the sparsification problem for sums

$F(S) = f_1(S) + \cdots + f_m(S)$ of symmetric submodular functions

${f_i}$ reduces to the sparsification problem for semi-norms:

$\tilde{F}(x) \mathrel{\mathop:}=\tilde{f}_1(x) + \cdots + \tilde{f}_m(x)$.

Importance scores

Let us consider now the sparsification problem \eqref{eq:ns}

for $p=1$.

As we discussed in previous lectures, a reasonable way of assigning

sampling probabilities is to take

for some random variable $\mathbf{Z}$ on $\R^n$, as this

represents the “importance” of the $i$th term $N_i(x)$ under the

distribution of $\mathbf{Z}$.

Let us also recall the notion of approximation we’re looking for:

Given the desired approximation guarantee, it’s natural to simply take

$\mathbf{Z}$ to be uniform on the unit ball

\[B_N \mathrel{\mathop:}=\{ x \in \R^n : N(x) \leqslant 1 \}\,.\]

For the purposes of analysis, it will be easier to take $\mathbf{Z}$ as

the random variable on $\R^n$ with density proportional to

$e^{-N(x)}$, but let us see that gives the same probabilities

\eqref{eq:ns-rhoi}

as averaging uniformly over $B_N$. To compare

the density $e^{-N(x)}$ and the density that is uniform on $B_N$, one

can take $\varphi_1(y)=e^{-y}$ and

\(\varphi_2(y) = \mathbf{1}_{\{y \leqslant 1\}}\) in the next lemma.

Lemma: Suppose that the density of the random variable $\mathbf{Z}$ is

$\varphi(N(x))$ for any sufficiently nice function $\varphi$. Then the

probabilities defined in \eqref{eq:ns-rhoi}

are independent of $\varphi$.

Proof: Define $V(r) \mathrel{\mathop:}=\mathrm{vol}_n(r B_N)$ and note

that $V(r) = r^n \mathrm{vol}_n(B_n)$. Let

$u : \R^n \to \R$ be a homogeneous function, i.e.,

$u(\lambda x) = |\lambda| u(x)$ for all

$\lambda \in \R, x \in \R^n$. Then we have

Recall that \(N(x) = N_1(x) + \cdots + N_m(x)\,,\) and $B_N$ is the unit

ball in the norm $N$. To apply our standard symmetrization/chaining

analysis, define the metric

where $\mathbf{Z}$ is the random variable with density $e^{-N(x)}$. Note

that this applies without any assumptions on $N$ because every norm is

$p$-uniformly smooth when $p=1$.

Recall that in this setting we take

$\rho_i = \frac{1}{n} \mathbb{E}[N_i(\mathbf{Z})]$,

therefore

We are left to prove \eqref{eq:max-ub}.

First, observe that the maximum need only be

taken over indicies $i$ in the set ${ \nu_1,\ldots,\nu_M }$. So we are

looking at the expected maximum of (at most) $M$ random variables. The

claimed upper bound follows immediately (see Problem 2(A) on Homework #2) from an

exponential concentration inequality:

Note that $N_i$ is only a small piece of the norm $N$, so there is

essentially no exploitable relationship between $N_i$ and $\mathbf{Z}$.

Therefore the concentration inequality will have to hold in some

generality.

Log-concave random vector: A random variable $\mathbf{X}$ on $\mathbb{R}^n$ is log-concave if

its density is $e^{-g(x)}\,dx$ for some convex function

$g : \mathbb{R}^n \to \mathbb{R}$.

Isotropic random vector:

A random variable $\mathbf{X}$ on $\mathbb{R}^n$ is isotropic if

$\mathbb{E}[\mathbf{X}]=0$ and

$\mathbb{E}[\mathbf{X} \mathbf{X}^{\top}] = I$.

Lipschitz functions: A function $\varphi: \mathbb{R}^n \to \mathbb{R}$ is $L$-Lipschitz

(with respect to the Euclidean distance) if

\[|\varphi(x)-\varphi(y)\| \leqslant L \|x-y\|_2\,, \quad \forall x,y \in \mathbb{R}^n\,.\]

Lemma [Gromov-Milman]: If $\varphi: \mathbb{R}^n \to \mathbb{R}$ is $L$-Lipschitz and

$\mathbf{X}$ is an isotropic, log-concave random variable, then

\[\begin{equation}\label{eq:kls-tail}

\mathbb{P}\left(|\varphi(\mathbf{X})-\mathbb{E}[\varphi(\mathbf{X})]| > t L\right) \leqslant e^{-c t/\psi_n}\,,\end{equation}\]

where $c > 0$ is an absolute constant and $\psi_n$ is the KLS constant

in $n$ dimensions.

Note that the KLS constant has many definitions that are equivalent up

to a constant factor, and one could take \eqref{eq:kls-tail} as the definition.

See links to related material at the end.

To prove \eqref{eq:ni-con}, first note that our random variable $\mathbf{Z}$

is log-concave because $N(x)$ is a convex function. To make it

isotropic, we define

$\mathbf{X} \mathrel{\mathop:}=A^{-1/2} \mathbf{Z}$, where

$A \mathrel{\mathop:}=\mathbb{E}[\mathbf{Z} \mathbf{Z}^{\top}]$.

We will apply the lemma to the map $\varphi(x) \seteq N_i(A^{1/2} x)$, and we

need only evaluate the Lipschitz constant of $\varphi$.

In Homework #2

problem 4, you show that $\varphi$ is $L$-Lipschitz with

$L \lesssim \mathbb{E}[N_i(\mathbf{Z})]$, yielding \eqref{eq:ni-con}.

when $\mathbf{Z}$ chosen uniformly (according to the volume measure on

$\mathbb{R}^n$) from the unit ball $B_N$.

A first important thing to

notice is that it suffices to sample according to a distribution

$\tilde{\rho}$ that satisfies $\tilde{\rho}_i \geq c \rho_i$ for all $i=1,\ldots,m$ and some constant $c > 0$.

This follows from the way the importances ${\rho_i}$ are used in our

analyses.

and that our sparsification bounds are in terms of entropy numbers $e_{h}(B_F, d_{\nu,\rho})$

with \(B_F \seteq \{ x \in \R^n : F(x) \leq 1 \}\). Note that for an approximation $\tilde{\rho}$ as above, we have

which implies $e_h(B_F, d_{\nu,\tilde{\rho}}) \leq \frac{1}{c} e_h(B_F, d_{\nu,\rho})$.

It is now well-understood how to (approximatley) sample from the uniform

measure on a convex body. (See JLLS21 and CV18.)

Theorem: There is an algorithm

that, given a convex body $A \subseteq \mathbb{R}^n$ satisfying

$r \cdot B_2^n \subseteq A \subseteq R \cdot B_2^n$ and

$\varepsilon> 0$, samples from a distribution that is within TV distance

$\varepsilon$ from the uniform measure on $A$ using

$O(n^3 (\log \frac{nR}{\varepsilon r})^{O(1)})$ membership oracle

queries to $A$, and $(n (\log \frac{nR}{\varepsilon r}))^{O(1)}$

additional time.

Say that a seminorm $N$ on $\mathbb{R}^n$ is $(r,R)$-rounded if it

holds that

\[r \|x\|_2 \leqslant N(x) \leqslant R \|x\|_2\,,\quad \forall x \in \ker(N)^{\perp}\,.\]

If $N$ is a genuine norm (so that $\ker(N)=0$) and $N$ is

$(r,R)$-rounded, then $r B_2^n \subseteq B_N \subseteq R B_2^n$, hence

we can use the theorem to sample and estimate. But even in this case the

running time for computing $\rho_1,\ldots,\rho_m$ would be

$\tilde{O}(m n^{O(1)} \log \frac{R}{r})$ since evaluating $N$ requires

$\Omega(m)$ time assuming each $N_i$ can be evalued in $O(1)$ time.

The homotopy method

Sparsification from sampling from sparsification. We would like a better running time of the form

$\tilde{O}(m + n^{O(1)}) \log \frac{R}{r}$.

Note that if we could compute approximations ${\tilde{\rho}_i}$ to the

importance scores, then we could sample from $\tilde{\rho}$, which would

allow us to sparsify to obtain an approximation $\tilde{N}$ to $N$ with only

$\tilde{O}(n)$ non-zero terms. This approximation could then be

evaluated in time $n^{O(1)}$, allowing us to obtain samples in only

$n^{O(1)}$ time. With these samples, we could then sparisfy.

To solve this “chicken and egg” problem, we use the following simple (but elegant)

method. Define, for $t > 0$,

\[N_t(x) \mathrel{\mathop:}=N(x) + t \norm{x}_2\,.\]

Assuming $N$ is an $(r,R)$-rounded semi-norm, it follows that

$N_R(x) \asymp R \norm{x}_2$.

As far as I know, in the context of \(\ell_p\) regression and sparsification vs. sampling, this “homotopy method”

originates from work of [Li-Miller-Peng 2013] . See also

the work of [Bubeck-Cohen-Lee-Li 2017].

Thus we can compute an \(\tilde{O}(n)\)-sparse $1/2$-approximation to

\(\tilde{N}_R(x)\) by sampling from the Euclidean unit ball. But now since

\(\tilde{N}_t(x) \asymp \tilde{N}_{t/2}(x)\) this allows us to obtain an

\(\tilde{O}(n)\)-sparse $1/2$-approximation \(\tilde{N}_{R/2}(x)\) of

\(N_{R/2}(x)\).

Doing this $O(\log \frac{R}{\varepsilon r})$ times, we eventually obtain

an $\tilde{O}(n)$-sparse $1/2$-approximation

\(\tilde{N}_{\varepsilon r}(x)\) of \(N_{\varepsilon r}(x)\).

We can use this to obtain an $\tilde{O}(n)$ sparse

$\varepsilon$-approximation to $N_{\varepsilon r}(x)$ which it self an

$\varepsilon$-approximation to $N(x)$ on $\ker(N)^{\perp}$, using the

assumption that $N$ is $(r,R)$-rounded.

Finally, we can easily remove the Euclidean shift from

\(\tilde{N}_{\varepsilon r}(x)\), yielding a genuine

$\varepsilon$-approximation to $N(x)$, since only the Euclidean part of

$\tilde{N}_{\varepsilon r}(x)$ has support on $\ker(N)$.

Empirical risk minimization (ERM) is a widely studied problem in

learning theory and statistics. A prominent special case is the problem

of optimizing a generalized linear model (GLM), i.e.,

where the total loss $F : \mathbb R^n \to \mathbb R$, is defined

by vectors $a_1,\ldots,a_m \in \mathbb R^n$, $b \in \mathbb R^m$,

and loss functions $f_1, \dots, f_m: \mathbb R\to \mathbb R$.

Different choices of the loss functions ${ \varphi_i }$ capture a

variety of important problems, including linear regression, logistic

regression, and $\ell_p$ regression.

When $m \gg n$, a natural approach for fast algorithms is to apply

sparsification techniques to reduce the value of $m$, while maintaining

a good multiplicative approximation of the objective value. This

corresponds to our usual sparsification model where

$f_i(x) = \varphi_i(\langle a_i,x\rangle - b_i)$. As mentioned

previously, we will can assume that $b_1=\cdots=b_m=0$ by lifting to one

dimension higher. In previous lectures, we solved the sparsification

problem when $\varphi_i(z)=|z|^p$ for some $1 \leqslant p \leqslant 2$.

However, $\ell_p$ losses are the only class of natural loss functions

for which linear-size sparsification results are known for GLMs. For

instance, for the widely-studied class of Huber-type loss functions, e.g., $\varphi_i(z) = \min(|z|, |z|^2)$, the

best known sparsity bounds obtained by previous methods were of the form

is $\tilde{O}(n^{4-2\sqrt{2}} \varepsilon^{-2})$.

We will often think of the case $\varphi_i(z) = h_i(z)^2$ for some

$h_i : \mathbb R\to \mathbb R_+$, as the assumptions we need are

stated more naturally in terms of $\sqrt{\varphi_i}$. To that end,

consider a function $h : \mathbb R^n \to \mathbb R_+$ and the

following two properties, where $L, c, \theta> 0$ are some positive

constants.

Assumptions:

($L$-auto-Lipschitz) $|h(z)-h(z’)| \leqslant L\,h(z-z’)$ for all

$z,z’ \in \mathbb R$.

(Lower $\theta$-homogeneous)

$h(\lambda z) \geqslant c \lambda^{\theta} h(z)$ for all

$z \in \mathbb R$ and $\lambda \geqslant 1$.

Theorem [Jambulapati-Lee-Liu-Sidford 2023]: Consider

$\varphi_1, \dots, \varphi_m: \mathbb R\to \mathbb R_{+}$, and

suppose there are numbers $L,c,\theta> 0$ such that each

$\sqrt{\varphi_i}$ is $L$-auto-Lipschitz and lower $\theta$-homogeneous

(with constant $c$). Then for any $a_1,\ldots,a_m \in \mathbb R^n$,

and numbers $0 < \varepsilon< \tfrac12$ and

$s_{\max}> s_{\min}\geqslant 0$, there are nonnegative weights

$w_1,\ldots,w_m \geqslant 0$ such that

Moreover, the weights ${w_i}$ can be computed in time

\(\tilde{O}_{L,c,\theta}\!\left((\mathsf{nnz}(a_1,\ldots,a_m) + n^{\omega} + m \mathcal{T}_{\mathrm{eval}}) \log(ms_{\max}/s_{\min})\right)\),

with high probability.

Here, $\mathcal{T}_{\mathrm{eval}}$ is the maximum time needed to

evaluate each $\varphi_i$, $\mathsf{nnz}(a_1,\ldots,a_m)$ is the total

number of non-zero entries in the vectors $a_1,\ldots,a_m$, and $\omega$

is the matrix multiplication exponent. “High probability” means that the

failure probability can be made less than $n^{-\ell}$ for any $\ell > 1$

by increasing the running time by an $O(\ell)$ factor.

It is not difficult to see that for $0 < p \leqslant 2$, the function

$\varphi_i(z) =

|z|^p$ satisfies the required hypotheses of . Additionally, the

$\gamma_p$ functions, defined as

for $p \in (0, 2]$, also satisfy the conditions. The special case of

$\gamma_1$ is known as the Huber loss.

To show that $\sqrt{\gamma_p}$ is $1$-auto-Lipschitz, it suffices to

prove that $\sqrt{\gamma_p}$ is concave. The lower growth bound is

immediate for $p > 0$.

Importance sampling and multiscale weights

Given

$F(x) = \varphi_1(\langle a_1,x\rangle) + \cdots + \varphi_m(\langle a_m,x\rangle)$,

our approach to sparsification is via importance sampling. Given a

probability vector $\rho \in \mathbb R^m$ with

$\rho_1,\ldots,\rho_m > 0$ and $\rho_1 + \cdots + \rho_m = 1$, we sample

$M \geqslant 1$ coordinates $\nu_1,\ldots,\nu_M$ i.i.d. from $\rho$, and

define our potential approximator by

As we have seen, analysis of this expression involves the size of

discretizations of the set

\(B_F(s) \mathrel{\mathop:}=\{ x \in \mathbb R^n : F(x) \leqslant s \}\)

at various granularities. The key consideration (via Dudley’s entropy

inequality) is how well $B_F(s)$ can be covered by cells on which we

have uniform control on how much the terms

$\varphi_i(\langle a_i,x\rangle)/\rho_i$ vary within each cell.

The $\ell_2$ case

Let’s consider the case $\varphi_i(z) = |z|^2$ so that

$F(x) = |\langle a_1,x\rangle|^2 + \cdots + |\langle a_m,x\rangle|^2$.

Here, \(B_F(s) = \{ x \in \mathbb R^n : \norm{Ax}_2^2 \leqslant s \}\),

where $A$ is the matrix with $a_1,\ldots,a_m$ as rows.

and the pertinent question is how many translates of $\mathsf K_j$ it

takes to cover $B_F(s)$. In the $\ell_2$ case, this is the well-studied

problem of covering Euclidean balls by $\ell_{\infty}$ balls.

If $N_j$ denotes the minimum number of such cells required, then the

dual-Sudakov inequality tells us that

Choosing

$\rho_i \mathrel{\mathop:}=\frac{1}{n} |(A^\top A)^{-1/2} a_i|_2^2$ to

be the normalized leverage scores yields uniform control on the size of

the coverings:

$$\log N_j \lesssim \frac{s}{2^j} n \log m\,.$$

The $\ell_p$ case

Now we take $\varphi_i(z) = |z|^p$ so that $F(x) = \norm{Ax}_p^p$. A cell

at scale $2^j$ now looks like

To cover $B_F(s)$ by translates of $\mathsf K_j$, we will again employ

Euclidean balls, and one can use $\ell_p$ Lewis weights to relate the

$\ell_p$ structure to an $\ell_2$ structure.

A classical result of Lewis

establishes that there are nonnegative weights

$w_1,\ldots,w_m \geqslant 0$ such that if

$W = \mathrm{diag}(w_1,\ldots,w_m)$ and

$U \mathrel{\mathop:}=(A^{\top} W A)^{1/2}$, then

If we are trying to use $\ell_2$-$\ell_{\infty}$ covering bounds, we

face an immediate problem: Unlike in the $\ell_2$ case, we don’t have

prior control on $\norm{U x}_2$ for $x \in B_F(s)$. One can obtain an

initial bound using the structure of $U = (A^{\top} W A)^{1/2}$:

where the last inequality is Cauchy-Schwarz:

$|\langle a_i, x\rangle| = |\langle U^{-1} a_i, U x\rangle| \leqslant\norm{U^{-1} a_i}_2 \norm{U x}_2$.

This gives the bound $\norm{U x}_2 \leqslant\norm{Ax}_p \leqslant s^{1/p}$ for

$x \in B_F(s)$.

Problematically, this uniform $\ell_2$ bound is too weak, but there is a

straightforward solution: Suppose we cover $B_F(s)$ by translates of

$\mathsf K_{j_0}$. This gives an $\ell_{\infty}$ bound on the elements

of each cell, meaning that we can apply

\eqref{eq:intro-nc0} and obtain a better upper bound on \(\norm{Ux}_2\)

for $x \in \mathsf K_{j_0}$. Thus to cover $B_F(s)$ by translates of

$\mathsf K_j$ with $j < j_0$, we will cover first by translates of

$\mathsf K_{j_0}$, then cover each translate

$(x + \mathsf K_{j_0}) \cap B_F(s)$ by translates of

$\mathsf K_{j_0-1}$, and so on.

The standard approach in this setting is to use interpolation

inequalities and duality of covering numbers for a cleaner analytic

version of such an iterated covering bound. But the iterative covering

argument can be adapted to the non-homogeneous setting, as we discuss

next.

Non-homogeneous loss functions

When we move to more general loss functions

$\varphi_i : \mathbb R\to \mathbb R$, we lose the homogeneity

property $\varphi_i(\lambda x) = \lambda^p \varphi_i(x)$, $\lambda > 0$

that holds for $\ell_p$ losses. Because of this, we need to replace the

single Euclidean structure present in \eqref{eq:wis}

(given by the linear operator $U$) with a family of structures, one for every relevant scale.

Definition (Approximate weight at scale $s$):

Fix $a_1,\ldots,a_m \in \mathbb R^n$ and loss functions

$\varphi_1,\ldots,\varphi_m~:~\mathbb R\to \mathbb R_+$. Say that a

vector $w \in \mathbb R_+^m$ is an $\alpha$-approximate weight at

scale $s$ if

Moreover, in order to generalize the iterated covering argument for

$\ell_p$ losses, we need there to be a relationship between weights at

different scales.

Definition (Approximate weight scheme):

Let $\mathcal J\subseteq \mathbb Z$ be a contiguous interval. A family

${w^{(j)} \in \mathbb R_+^m : j \in \mathcal J}$ is an

$\alpha$-approximate weight scheme if each $w^{(j)}$ is an

$\alpha$-approximate weight at scale $2^j$ and, furthermore, for every

pair $j,j+1 \in \mathcal J$ and $i \in {1,\ldots,m}$,

Recall the definitions of approximate weights and weight schemes from

the previous lecture.

Theorem 1: Suppose that $\varphi_1,\ldots,\varphi_m : \mathbb R\to \mathbb R_+$

are lower $\theta$-homogeneous and upper $u$-homogeneous with

$u > \theta> 0$ and uniform constants $c, C > 0$. Then there is some

$\alpha = \alpha(\theta,c,u,C) > 1$ such that for every choice of

vectors $a_1,\ldots,a_m \in \mathbb R^n$ and $s > 0$, there is an

$\alpha$-approximate weight at scale $s$.

This can be proved by considering critical points of the functional

$U \mapsto \det(U)$ subject to the constraint $G(U) \leqslant s$, where

analogous to how we showed the existence of Lewis weights.

Theorem 2: Suppose that $\varphi_1,\ldots,\varphi_m : \mathbb R\to \mathbb R_+$

are lower $\theta$-homogeneous and upper $u$-homogeneous with

$4 > u > \theta> 0$ and uniform constants $c, C > 0$. Then for every

choice of vectors $a_1,\ldots,a_m \in \mathbb R^n$, there is an

$\alpha$-approximate weight scheme \(\{ w_i^{(j)} : j \in \mathbb Z\}\).

Contractive algorithm

For a full-rank matrix $V$ with rows $v_1,\ldots,v_m \in \mathbb R^n$,

define the $i$th leverage score of $V$ as \(\label{eq:ls-def}

\sigma_i(V) \mathrel{\mathop:}=\langle v_i, (V^{\top} V)^{-1} v_i\rangle\,.\)

For a weight $w \in \mathbb R_{+}^m$ and \(i \in \{1,\ldots,m\}\),

define

\(\tau_i(w) \mathrel{\mathop:}=\frac{\sigma_i(W^{1/2} A)}{w_i} = \langle a_i, (A^{\top} W A)^{-1} a_i\rangle\,, \quad W \mathrel{\mathop:}=\mathrm{diag}(w_1,\ldots,w_m)\,,\)

and denote $\tau(w) \mathrel{\mathop:}=(\tau_1(w),\ldots,\tau_m(w))$.

Fix a scale parameter $s > 0$ and define the iteration

$\Lambda_s : \mathbb R_+^m \to \mathbb R_+^m$ by

Write $\theta^k \mathrel{\mathop:}=\theta \circ \cdots \circ \theta$ for

the $k$-fold composition of $\theta$. In this case where

$\varphi_i(z)=|z|^p$ and $1 \leqslant p \leqslant 2$, it is known, for

$s = 1$, starting from any $w_0 \in \mathbb R_{+}^m$, the sequence

\(\{\Lambda_1^k(w_0) : k \geqslant 1\}\) converges to the unique fixed

point of $\varphi$, which are the corresponding $\ell_p$ Lewis weights.

Fact: A vector

$w \in \mathbb R_+^m$ is an $\alpha$-approximate weight at scale $s$

if and only if \(d(w,\Lambda_s(w)) \leqslant\log \alpha\,.\)

First, we observe that $\tau$ is $1$-Lipschitz on

$(\mathbb R_+^m, d)$. In the next proof, $\preceq$ denotes the

ordering of two real, symmetric matrices in the Loewner order, i.e.,

$A \preceq B$ if and only if $B-A$ is positive semi-definite.

Lemma: For

any $w,w’ \in \mathbb R_{+}^m$, it holds that

$d(\tau(w), \tau(w’)) \leqslant d(w,w’)$.

Proof:

Denote $W = \mathrm{diag}(w), W’ = \mathrm{diag}(w’)$, and

$\alpha \mathrel{\mathop:}=\exp(d(w,w’))$. Then

$\alpha^{-1} W \preceq W’ \preceq \alpha W$, therefore

$\alpha^{-1} A^\top W A \preceq A^\top W’ A \preceq \alpha A^\top W A$,

and by monotonicity of the matrix inverse in the Loewner order,

$\alpha^{-1} (A^\top W A)^{-1} \preceq (A^\top W’ A)^{-1} \preceq \alpha (A^\top W A)^{-1}$.

This implies $d(\tau(w),\tau(w’)) \leqslant\log \alpha$, completing the

proof.

Proof of Theorem 2

Consider the map $\psi: \mathbb R_+^m \to \mathbb R_+^m$ whose

$i$-th coordinate is defined as

Fix $s > 0$ and consider the mapping

$\varphi: \mathbb R_+^m \to \mathbb R_+^m$ defined in \eqref{eq:phi-iter}

Then for $u< 4$ and

$\delta \mathrel{\mathop:}=\max \left(\left|\frac{\theta}{2}-1\right|, \left|\frac{u}{2}-1\right|\right) < 1$,

in conjunction with \eqref{eq:psi-contract}, shows that

Now define \(w^{(0)} \mathrel{\mathop:}=\varphi^{k}_{1}(1,\ldots,1)\,,\)

where $k \geqslant 1$ is chosen large enough so that

$d(w^{(0)}, \Lambda_{1}(w^{(0)})) \leqslant\frac{2 \log C_1}{1-\delta}$.

From , one sees that $w^{(0)}$ is an $\alpha$-approximate weight at

scale $1$ for $\alpha = C_1^{2/(1-\delta)}$.

where the last inequality uses $\Lambda_{2s}(w) = 2 \Lambda_s(w)$ for all

$w \in \mathbb R_+^m$.

Therefore, by induction,

$d(\Lambda_{2^j}(w^{(j)}), w^{(j)}) \leqslant\frac{2 \log(C_1) + \log 2}{1-\delta}$

for all $j > 0$. To see that the family of weights

\(\{ w^{(j)} : j \in \mathbb Z\}\) forms a weight scheme, note that

These are preliminary notes for analyzing the Ito process.

Reis and Rothvoss gave an algorithm

for finding BSS sparsifiers that uses

a a discretized random walk. It appears conceptually simpler to

use a modified Brownian motion directly.

Consider symmetric matrices $A_1,\ldots,A_m \succeq 0$ with

$|A_1|+\cdots+|A_m| \preceq \mathbb{I}_n$. Define a stochastic

process $X_t = (X_t^1,\ldots,X_t^m)$ by $X_0 = 0$, and

$$dX_t = \mathbb{I}_{\mathcal J_t}\, dB_t\,,$$

where \(\{B_t\}\) is a standard Brownian motion and

\(\mathcal J_t \subseteq [m]\) is the set of good coordinates at time \(t\).

Define the stopping times

\(T_i \mathrel{\mathop:}=\inf \{ t > 0 : |X_t^i| \geqslant 1 \}\) and the

set of stopped coordinates

$$\mathcal S_t \mathrel{\mathop:}=\{ i \in [m] : T_i \leqslant t \}\,.$$

We will ensure that \(\mathcal J_t \cap \mathcal S_t = \emptyset\) so that

\(|X_t^1|,\ldots,|X_t^m| \leqslant 1\) holds for all times

\(t \geqslant 0\).

Denote

\(T \mathrel{\mathop:}=\sup \{ t > 0 : |\mathcal S_t| \leqslant m/2 \}\).

Our goal is to show that with good probability,

$$\label{eq:goal}

\sum_{i=1}^m X_T^i A_i \preceq C \left(\frac{n}{m}\right)^{1/2} \mathbb{I}_n\,.$$

Since the stopping time \(T\) entails that \(m/2\) coordinates have been

fixed to \(\pm 1\), this completes the argument since at least one of the

two matrices \(\sum_{i=1}^m (1+X_T^i) A_i\) or

\(\sum_{i=1}^m (1-X_T^i) A_i\) has at most \(m/2\) non-zero coefficients,

and

Repeatedly halving \(m\) until \(m \asymp n/\varepsilon^2\) yields a

\(1 \pm \varepsilon\) approximation with \(O(n/\varepsilon^2)\) sparsity. To

get a two-sided bound, replace \(A_i\) by

\(\begin{pmatrix} A_i & 0 \\ 0 & - A_i\end{pmatrix}\).

To this end, let us define, for parameters $\theta,\lambda > 0$ to be

chosen later,

Define $U_t \mathrel{\mathop:}=U(X_t)$. Note that

$\Phi(X_0)=\Phi(0) = n/\theta$ and $U_0 \succ 0$. The idea is that if

${ \Phi(X_t) : t \in [0,T] }$ remains bounded, then $U_t \succ 0$

holds for $t \in [0,T]$, and therefore at time $T$,

The blue terms are the martingales, which we ignore for the moment. The

green terms are error terms. The two red terms need to be balanced by

choosing $\theta,\lambda$ appropriately.

For any $A,B$ with singular values

$\sigma_1(A) \geqslant\cdots \geqslant\sigma_n(A)$ and

$\sigma_1(B) \geqslant\cdots \geqslant\sigma_n(B)$, we have

$$\mathop{\mathrm{tr}}(A B) \leqslant\sum_{i=1}^n \sigma_i(A) \sigma_i(B)\,.$$

In particular, if $A,B \succeq 0$, then

$\mathop{\mathrm{tr}}(AB) \leqslant\mathop{\mathrm{tr}}(A) \mathop{\mathrm{tr}}(B)$.

For $\gamma \mathrel{\mathop:}=8$, we have

$|\mathcal J_t| \geqslant m - |\mathcal I_t| - |\mathcal S_t| \geqslant\frac{m}{2} - \frac{m}{\gamma} \geqslant\frac{m}{4}$.

So let us take